Blog & Whitepapers

Download

2014

HOW TO COPE WITH NEW CHALLENGES FOR SMS TERMINATION?

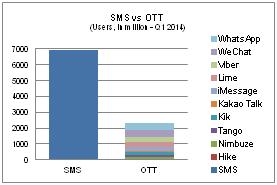

SMS vs OTT: has the match really started?

SMS is a $100+ billion business - Messaging is the biggest 'non voice' mobile service and it is growing. SMS accounts for almost half of the revenues generated by mobile messaging: it is a $100+ billion business for at least the next 3 years according to Portio Research. We now have 6.9 billion mobile subscriptions worldwide. The OTT messaging platforms, put all together, have a consolidated base of 2.3 billion users. WhatsApp, which is a massive success story, has “only” 450 million users!

Why you should pay premium/special attention to premium rate services billing ?

Premium Rate Services (PRS) are high-tariff services which account for 2 to 4 % of the annual mobile operator revenues (European average). Surprisingly, PRS billing is hardly monitored today despite customer complaints due to the lack of tariff awareness and / or billing errors. PRS also squeeze the operator margin due to the high costs charged by PRS partners. Any error can be immediately turned into a cash machine by professional fraudsters that constantly monitors the market.

Retail billing of PRS requires special monitoring because the charging principles are more complex and may include: flat fee rates, time-dependent rates (including a minimum/maximum charge per call), variable rates (depending on options selected by the subscriber), fees for additional services, special VAT schemes, etc.

Moreover PRS are usually outside the core package rate plans which result in limited testing and in billing errors being undetected. This may have a huge impact, e.g. a mobile operator in Europe recently had to refund €1.9 million to subscribers who had been billed incorrectly for 3 years for calls made to third-party premium rate numbers.

NEW EVOLUTIONS IN BYPASS FRAUD

How do you effectively tackle bypass fraud today?

Bypass fraud is still a major concern for mobile operators worldwide. Far from having disappeared, fraudsters have developed new techniques to protect their 'business'. They have implemented tactical responses against the main detection methods: (a) Profiling analysis performed in Fraud Management System, (b) Tracking campaigns based on Test Call Generation.

DATA SERVICE BILLING VERIFICATION

4G LTE: risk higher than ever for lost revenues?

4G LTE is now starting to drastically change the use of mobile data services. But, while mobile data traffic is growing exponentially, revenues paid by subscribers are either flat or declining due to intense competition. “How to price and bill for data services?” is still the most important issue which mobile operators are facing today!

Data transactions are currently usually rated and charged by volume; 'unlimited' data plans are still very popular even if operators are keen to phase them out. Operators are also experimenting with alternative models e.g. pricing by event or by duration of usage. On top of this, they often also promote the use of data services passes for infrequent data users or roamers. More recently, other sophisticated data plans are emerging in the market, such as tiered-data plans, application-based models, service bundles, turbo boost, device-based plans, shared data bundles,...

As pricing and billing strategies are becoming more complicated and diverse in an attempt to maximise revenues from data services, new risks must be addressed by the operators: